A global pandemic, a recession, social isolation, protests against racial injustice, political unrest. No matter how you look at it, 2020 was a gut punch. For credit unions and banks, the pandemic brought new challenges and exacerbated existing ones, from working remotely, to a flood of new deposits, to historically low rates (again).

As credit unions and banks look ahead to a post-pandemic recovery and figure out how to move forward, it’s important to take stock of what happened in 2020 — and what lessons this past year taught us.

Awash in stimulus money

Consumers may have happily welcomed three rounds of federal stimulus money since March 2020, but that created a challenge for credit unions and banks already dealing with record-low interest rates. On the one hand, stimulus checks translated into deposit growth as some customers simply parked these funds in bank accounts, awaiting their next move. With so much normal activity on hold for the last year, that money could be on its way out the door as consumers start to spend again (hello, European vacation). Credit unions and banks need to maintain flexible liquidity.

On the other hand, some people used their stimulus checks to pay off loans, causing loans to disappear from credit union and bank balance sheets even more. And as consumers’ spending habits changed, organic loan originations were sluggish.

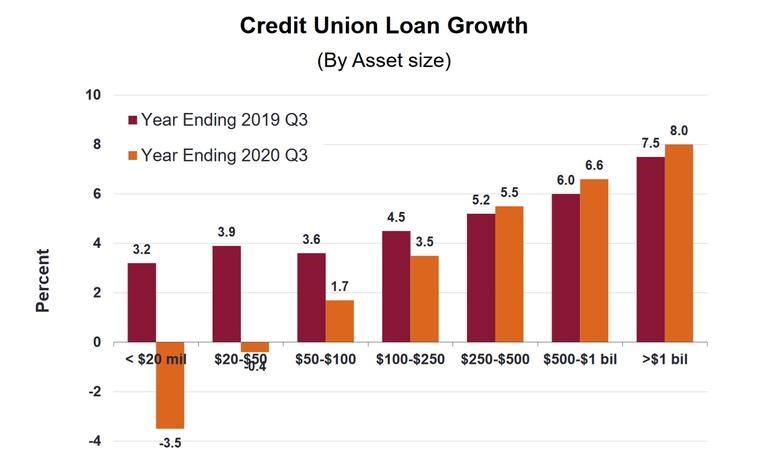

Loan growth takes a dive

Not surprisingly, the combination of stimulus money and a more conservative financial posture meant that consumers weren’t in the mood to borrow — at least not for anything that wasn’t a refi.

Loan growth climbed just 5.2% in 2020, well below the long-term average of 7.2% and the slowest pace in six years, according to CUNA Mutual. But most of the decline was experienced by small players. Credit unions with assets of more than $1 billion saw 8% growth but those with assets under $20 million fell 3.5%, compared to a 3.2% rise the previous year. Larger players must now be mindful that even though they had decent originations in 2020, it was due to the refi boom. Loan growth could still be a struggle once the refi frenzy abates.

Low interest rates as far as the eye can see

The Federal Reserve wasted no time in responding to the Covid-19 economic downturn, coming out with a series of actions, including a cut to the Fed target rate. For lenders, 2020 was marked by a massive refi boom, though that has calmed somewhat. Thirty-year fixed rate mortgages dipped down to 2.68% and 15-year loans even lower. What’s more, the Fed has vowed to keep rates near zero for the foreseeable future, at least until the economy recovers fully.

Despite the refinancing activity, credit unions and banks realized they need more sustainable sources of loan originations with higher margins. Even if refis help boost your loan originations, there’s no advantage to loading up the balance sheet with sub-3% mortgages.

And with rates going back up now, refis are slowing, so even that source of originations is evaporating. And consider that the many of the 2020 mortgages will wind up in the hands of government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. What will be your source of sustainable originations going forward?

The wild card: Student loans

With layoffs and financial hardship mounting, the Department of Education moved quickly to provide borrowers with relief. Many of those early provisions, such as a temporary suspension of payments and interest-free loans for federal student loans, are still in place through at least Sept. 30, 2021. The number of student loans in forbearance doubled during Covid. That creates uncertainty about what will happen when payments resume on Oct. 1. Will there be a payment shock that ripples out to other obligations?

If what we’ve seen from private lenders is any indication, perhaps not. While federal student loan provisions don’t apply to loans held by credit unions and banks, many borrowers with private loans also requested loan extensions, deferments and forbearance during Covid. The good news: recent reports from private lenders suggest that as borrowers have come out of forbearance, those loans performed strongly in repayment. That’s a good sign for the asset class.

How to move forward

Even though 2020 is over, there are still lingering effects. Today’s market may not be what you’re used to, but there’s no going back to pre-pandemic banking. CFOs and finance departments need to plot a new course. Here are a few ways to do that:

- Focus on the balance sheet. With low interest rates and anemic loan originations, credit unions and banks need to rethink their approach to balance sheet management, including improving loan retention, expanding partnerships, and shedding long-term, low-rate mortgages. We offer up tips for better balance sheet management in a recent blog post.

- Beware of interest margin squeeze. Expect interest rates to stay low and balance sheets to stay flush with deposits. You’ll want to seek out reliable sources of non-interest income to hedge against interest margin compression. Loan participations are a way to access shorter-term products with higher yields.

- Diversify your loan portfolio. Mortgages and auto loans may be the bread and butter of consumer lending, but an overreliance on this type of borrowing can box you in. Consider looking in areas of the market where there’s economic activity, like RVs and home improvement loans. On the other hand, if your institution has too many RV and home improvement loans, think about diversifying into more traditional debt. Innovations in loan participations have made it easier than ever for credit unions and banks to access new, diversified assets without the hassle of in-house origination. Check out our Next Generation Guide to Loan Participations for more information.

All signs point to a recovery, but it’s still early days. Credit unions and banks can’t let up just yet. They still need to stay agile. The lessons learned from 2020 will be your roadmap for what lies ahead.